Oil & Gas Markets

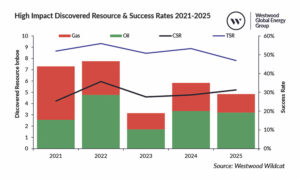

Westwood: Decline in exploration drilling continued in 2025, with only 64 high-impact wells drilled

The industry saw a 17% drop in the number of high-impact exploration wells drilled in 2025 compared with the year prior. Moreover, those 64 wells represent the lowest annual total recorded by Westwood Global Energy Group since 2008. The company’s State of Exploration 2026 report, issued in June, stated that the 64 wells delivered 4.8 billion barrels of oil equivalent (boe) of discovered resource at a 31% commercial success rate (CSR).

Key discoveries were made at Bumerangue in the pre-salt Lower Cretaceous carbonate play in the Santos Basin Brazil, at Mopane-3X and Capricornus in the Upper and Lower Cretaceous plays in Namibia’s Orange Basin, as well as the Hai Su Vang discovery in the Oligocene sandstone play in Vietnam’s Cuu Long Basin. Key failures were drilled in the Niger Delta, Suriname-Guyana, Herodotus, Andaman and Ulleung basins.

Over the five-year period from 2021-2025, 373 high-impact wells delivered approximately 29 billion boe of potentially commercial resource at a 30% CSR. The five-year trends show the industry moving further into deeper water, with 16% of wells drilled in ultra-deepwater in 2025. Only two of the 37 wells completed in ultra-deepwater between 2021-2025 made a commercial discovery (5% CSR) despite technical success rates being in line with other water depths. The two discoveries were at Venus in Namibia’s Orange Basin and Megah in Malaysia’s Sabah Basin.

Although frontier play drilling has been steady in recent years, CSRs remain low, averaging 13% over the last five years. The scale of the 38 new plays opened in the past 15 years is generally modest, with a median play size of around 500 million boe. Only 15 emerging play wells were drilled in 2025.

Further, only eight of the 38 new plays opened since 2011 have proved to be greater than 1 billion boe. In more than half the new plays, more than 90% of total play resource is captured in the opening discovery, with generally limited running room for follow-on drilling.

Supermajors and national oil companies continue to dominate high-impact exploration, accounting for eight of the 10 most active explorers in 2021-2025 and 65% of high-impact well equity in 2025. The role of the small and medium companies has diminished over the past decade, shrinking from 26% of the equity in 2016 to 16% in 2025. Supermajors discovered 36% of the overall resource in 2025, although small companies delivered a better success rate at around 35%.

Wood Mackenzie: Impact of UAE exit from OPEC likely won’t be seen until 2027

The United Arab Emirates’ withdrawal from OPEC, effective 1 May 2026, represents the most significant fracture in the organization’s 66-year history and increases the risk of oversupply weakening prices, according to Wood Mackenzie analysis.

The UAE, which joined OPEC in 1967 and grew to become the group’s second-largest producer by liquids capacity, announced its departure on 28 April. The country’s Ministry of Energy and Infrastructure said the decision follows a review of production policy and capacity outlook and aligns with its strategy to accelerate domestic energy investment. Before its exit, the UAE accounted for around 14% of OPEC capacity.

The country has committed $145 billion to its domestic upstream oil sector over the decade to 2030. Its overarching goals are to expand oil production capacity from under 4 million barrels per day (bpd) in 2020 to 5 million bpd by 2027. By 2024, capacity had already reached 4.85 million bpd.

“The UAE’s departure from OPEC will have minimal impact on market fundamentals in 2026, even if the Strait of Hormuz reopens,” said Simon Flowers, Chairman and Chief Analyst at Wood Mackenzie. “Gulf countries, including the UAE, will take months to return to pre-war production volumes. Beyond this year, losing the UAE will compound OPEC’s challenge to balance the market and increase the risk of oversupply weakening prices.”

By 2027 and beyond, the UAE will have the capability to take a growing share of global oil demand, which challenges OPEC’s current policy of unwinding its voluntary cuts. If tensions escalate, competition between the UAE and OPEC for market share could send medium-term oil prices sharply lower.

“The capacity-quota dispute reflects deeper political fractures, and tensions between Saudi Arabia and the UAE have been steadily building,” Mr Flowers said. “The UAE has much lower fiscal oil price breakevens relative to its peers, leaving its economy relatively resilient and better able to sustain a potential period of low prices.”