Wood Mackenzie: Current investment levels sufficient to meet oil and gas demand in 2030s

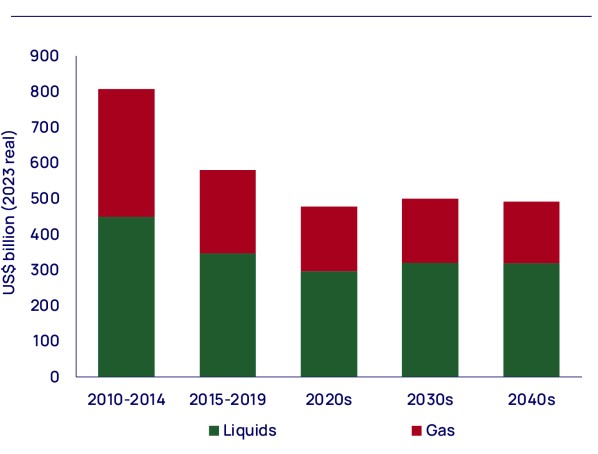

Despite concerns about underinvestment in upstream, peak oil and gas demand can be met in the 2030s without a substantial increase to current annual investment levels of $500 billion, according to a new report from Wood Mackenzie.

Current upstream spending is a little more than half of the $914 billion 2014 peak (in 2023 terms), according to the report (“Doing More With Less: Debunking the Myth of Upstream Underinvestment”). This apparent shortfall has fed a widespread belief that the industry is underinvesting and that a supply crunch is inevitable, be it sooner or later.

However, Fraser McKay, Head of Upstream Analysis, said this was never Wood Mackenzie’s opinion: “Our long-held view has been that spending and supply would rise to meet recovering demand and that the upstream industry would not and could not reprise the ignominious years of ‘peak inefficiency’ during the early 2010s.”

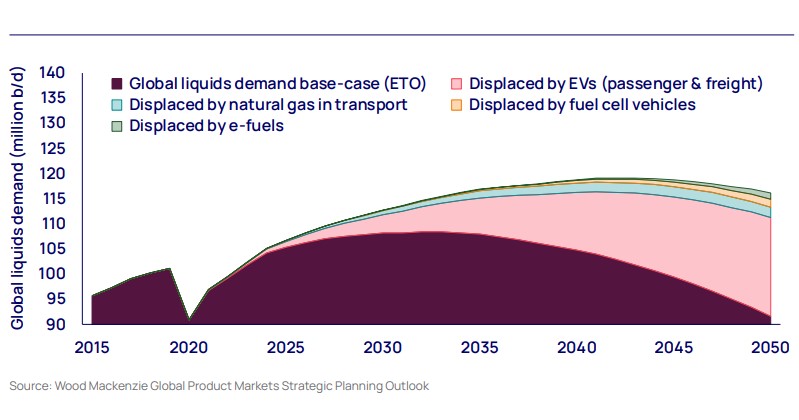

With oil demand bouncing back from pandemic lows, Wood Mackenzie predicts it will eclipse pre-pandemic highs in 2023. From 2024, oil demand growth will slow, reaching a peak of 108 million bbl/day in the early 2030s.

Spending levels not much higher than the current run-rate can deliver the supply needed to meet demand through to its peak and beyond. The report noted three reasons for this: the development of giant low-cost oil resources, relentless capital discipline and a transformational improvement in investment efficiency. Adversity was the primary catalyst for a structural change in supply efficiency. The price shocks of 2015-2016 and 2020-2021 forced the industry to become far more disciplined with its capital.

“Conventional greenfield unit development costs have been slashed by 60% in 2023 terms” Mr McKay said. “US tight oil wells generate nearly three times more production today for the same unit of capital than in 2014. New technology, capital efficiency and modularisation have been leveraged to powerful effect.”

According to the report, most of the industry’s oil and gas investment for the rest of this decade will target advantaged resources: those with the lowest cost, lowest emissions and least risk. Beyond that, new supply will become more expensive to develop. To meet demand, the industry will depend increasingly on late-life reserves growth from legacy supply sources, higher-cost greenfield developments and as yet undiscovered volumes.

But there are alternative demand scenarios, each with vastly different implications for future upstream investment. And there are risks to the required investment showing up. Efficiency and investment will evolve and the ‘required’ equilibrium is unlikely to play out.

Upstream spending levels required to meet our base-case ETO demand outlook. (Source: Wood Mackenzie Upstream Service)

Wood Mackenzie’s base-case Energy Transition Outlook (ETO) is equivalent to a 2.5 °C pathway, but even in its Accelerated Energy Transition outlook for a 1.5 °C trajectory, substantial investment is still required. Wood Mackenzie calculates nearly $400 billion per year would be required in the 2020s and nearly $250 billion a year in the 2030s (in 2023 terms).

The impacts of underinvestment would be far-reaching, with consequences for the global economy. But Wood Mackenzie believes that sustained investment imbalances are unlikely to persist.

“This cycle is certainly different. Energy transition uncertainty adds a new layer of complexity and risk for upstream investors. But the oil market is literally and metaphorically liquid. Price signals, reinvestment rates and the actions of OPEC+ eventually bring demand and supply back into balance,” Mr McKay said.