Oil & Gas Markets

Westwood: M&A deals and new drilling plans likely to keep global onshore rig demand on upward trend

Several big M&A deals were announced in this quarter, including the merger of Patterson-UTI and NexTier, forming a $5.4 billion oilfield services company. The UK’s INEOS Energy also entered the US market with its purchase of 172,000 acres of Chesapeake Energy’s Eagle Ford shale assets. In Canada, ConocoPhillips purchased TotalEnergies’ 50% stake in the Surmont oil sands. In Latin America, Seacrest Petróleo acquired Petrobras Norte Capixaba’s onshore assets, establishing itself as the third-largest onshore oil and gas producer in Brazil.

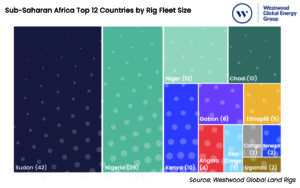

Several drilling campaigns also recently secured funding, signifying renewed interest in onshore projects. For example, ConocoPhillips announced it had approved funding for the development of the Nuna project in the Kuparuk River Unit in Alaska. The drilling campaign is expected to begin after pipeline installation is completed next year, with first oil in early 2025. Another example is Invictus Energy, which raised $12.7 million in capital to begin the next phase of drilling the Mukuyu-2 appraisal well in the Cabora Bassa basin of Zimbabwe. Exalo’s 202, a 1,200-hp rig, has been contracted to drill the well.

Also in Africa, TotalEnergies is now planning to kick off its delayed drilling campaign at the OML 58 onshore block in Nigeria. Drilling is expected to begin in 2024 and last for two to three years.

In Ghana, the Ghanaian National Petroleum Corp (GNPC) plans to start its onshore exploration program in the Voltaian Basin in 2024. GNPC has been building capacity for exploration since 2017. It will tender for a rig in late 2023 or 2024.

In Latin America, Gran Tierra Energy and Ecopetrol agreed to a 20-year extension for the Suroriente Block. A novel term was added in the contract that allows for long-term investment in work programs and infrastructure to boost oil recovery efficiency in existing fields, as well as the incorporation of appraisal drilling. Gran Tierra has committed to a $123 million capital investment program for the block.

Activity also remained strong in the Gulf Cooperation Council region, with multiple contracts awarded in Oman, UAE and Kuwait for work scopes encompassing well intervention, water/gas injection, and rig equipment servicing.

Is the oil and gas industry really underinvesting? Wood Mackenzie says no

Despite concerns about underinvestment in upstream, peak oil and gas demand can be met in the 2030s without a substantial increase to current annual investment levels of $500 billion, according to a recent report from Wood Mackenzie.

Current upstream spending is a little more than half of the 2014 peak of $914 billion (in 2023 terms), according to the report. This shortfall has led to the industry’s belief that it is underinvesting.

“This was never Wood Mackenzie’s opinion” said Fraser McKay, Head of Upstream Analysis for Wood Mackenzie. “Our long-held view has been that spending and supply would rise to meet recovering demand and that the upstream industry would not and could not reprise the ignominious years of ‘peak inefficiency’ during the early 2010s.”

From 2024, Wood Mackenzie predicts oil demand growth will slow, reaching a peak of 108 million bopd in the early 2030s.

The firm cited three main reasons for why it believes that spend levels not much higher than the current run-rate can deliver the supply needed to meet demand through to its peak and beyond: the development of giant low-cost oil resources, relentless capital discipline and a transformational improvement in investment efficiency.

“Conventional greenfield unit development costs have been slashed by 60% in 2023 terms” Mr McKay said. “And US tight oil wells generate nearly three times more production today for the same unit of capital than in 2014. New technology, capital efficiency and modularization have been leveraged to powerful effect.”

Most of the industry’s oil and gas investment for the rest of this decade will target advantaged resources: those with the lowest cost, lowest emissions and least risk. Beyond that, new supply will become more expensive to develop.

“Counterintuitively, the half-a-trillion run rate will need to be maintained beyond peak demand,” Mr McKay said.

Wood Mackenzie calculates nearly $400 billion per year would be required in the 2020s and nearly $250 billion a year in the 2030s (in 2023 terms).