Wood Mackenzie: Low oil prices put pressure on governments to alter upstream fiscal terms

A new two-part study by Wood Mackenzie details the implications of the current low oil price for upstream fiscal terms. Governments dependent on oil taxation income are wrestling with lower oil revenues for public spending and pressure from oil and gas companies for more lenient terms. While companies seek to reduce industry costs to levels compatible with the current oil price, they are also seeking a return to more lenient fiscal terms from host governments that have increased tax rates since 2005. Wood Mackenzie has identified a number of factors that will significantly influence whether a government will effect change. Central to this dilemma is how long the current low oil price will sustain: Is this a short-term blip, or are we witnessing structural change to the industry?

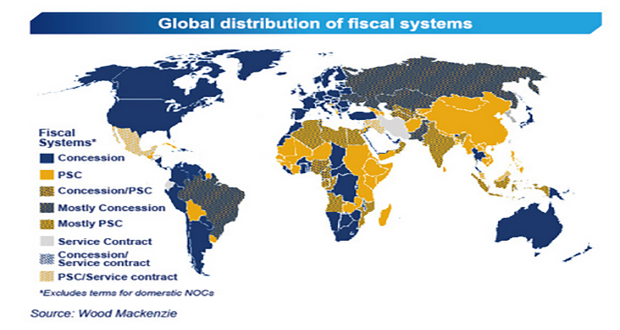

The six key factors that Wood Mackenzie claims will have a significant influence on whether a country is likely to change its fiscal terms under the current price environment are:

- Are the fiscal terms making projects uneconomic?

- Is the tax rate too high?

- Are there legal constraints on changing the terms?

- Is there a history of fiscal changes?

- Is the government dependent on oil taxation?

- What is the trend in oil production?

“Fiscal policymakers around the world are reviewing their upstream fiscal terms, and we’ve already witnessed changes to terms by a handful of governments since the price began to fall in 2014,” Graham Kellas, Vice President Global Fiscal Research for Wood Mackenzie, said. “For some governments, the impact the lower price has been devastating for public spending plans, especially those forged on oil price expectations of $100 a barrel, forcing them to slash spending with significant economic and political fallout.”

“The oil revenue ‘cake’ has shrunk, and it is hard for governments reliant on oil tax revenue to agree to a smaller slice of what’s left. But if they don’t offer better terms, the industry may simply stop investing. In these countries, the inclination will be to increase the government’s share of oil revenue to support its budget. This will make new investment in the country appear even less attractive than the lower price has done already,” Mr Kellas added.

“Many governments will be waiting to see if the lower price becomes established, reflecting a structural change in the industry. If so, there will be considerable pressure to revise applicable terms, but if the price continues to progress toward high levels ($80/bbl and above), then this pressure will be significantly alleviated.”

Wood Mackenzie’s analysis of fiscal changes from 2014 to date concludes that, while there has been much talk of fiscal change in response to low oil prices, only a few governments have followed through. The most notable example is the UK, which has made the most extensive changes, encompassing all assets. “Governments which are less dependent on oil tax for income can afford to play the long game and will be more likely to reduce tax rates or introduce incentives to try to maintain investment while companies cut back on new projects elsewhere,” Mr Kellas said. “However, their ability to do this may be restricted by contracts with oil & gas operators which insist that the fiscal terms remain as they are.”

Regressive fiscal terms – such as royalty, export duty, cost recovery ceilings and indirect taxes – have the most negative impact on future investment decisions. These are the most obvious targets for fiscal changes, especially in systems where the minimum government share of revenue is particularly high. Equally, high marginal tax rates reduce companies’ interest in incremental opportunities and may need to be lowered, or other allowances introduced.

“It’s important to note that governments facing declines in oil production would be considering how they can stimulate investment in any circumstances, and depressed oil prices makes this task more difficult and more necessary. Indonesia, in particular, may need to offer more attractive terms to try and stem its expected decline in oil production. Fiscal incentives for new investment – particularly challenging projects such as unconventional resources – are likely to become common,” Mr Kellas said.

Wood Mackenzie’s study shows several countries were already in the process of reviewing their fiscal terms before the oil price plunge, but this is an added complexity. “Governments now launching exploration licensing rounds face stiff competition in what is a buyers’ market,” Mr Kellas said. “The fiscal terms on offer will play a critical role in determining how attractive the opportunities are perceived.”