Rising demand, leaner rig fleet set stage for tighter offshore markets in 2024

Utilization and dayrates both forecast to edge up next year, driven by floater demand in Golden Triangle and jackup demand in Middle East

By Stephen Whitfield, Associate Editor

The global offshore rig market has finally started to climb out from the depths of the last oil price downturn and can expect to see some key metrics edging up in the next year.

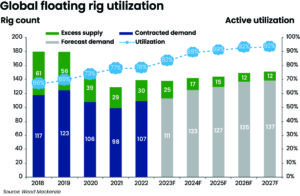

On the floater side, Wood Mackenzie forecasts the total number of active rigs will rise from 111 in 2023 to 123 in 2024, which would be the same level that was seen in 2019. However, while that 123 rigs translated to just 69% utilization in 2019, in 2024 that will be a much healthier utilization rate of 88%, due to a smaller overall fleet size. That compares with 82% utilization this year.

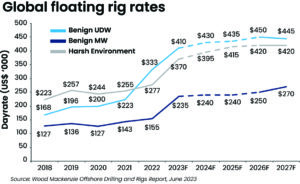

Average dayrates, too, will see slight increases. Wood Mackenzie forecasts benign shallow-water floaters will average $250,000 in 2024, up from $240,000 this year. Benign ultra-deepwater floaters will go up from $410,000 to $430,000, while harsh-environment floaters will go up from $370,000 to $390,000.

At the same time, the global marketed floater count is still below pre-downturn levels. Wood Mackenzie forecasts the number of marketed floating rigs will increase by just eight units next year, going from 141 to 149. That would still be a far cry from the 179 marketed rigs seen in 2019.

This drop in marketed supply reflects a new reality in the market, said Leslie Cook, Upstream Supply Chain Analyst at Wood Mackenzie. Drilling contractors remain reluctant to add new capacity due to issues like cost inflation and because operators have maintained capital discipline and strategies that favor short-cycle barrels. This means drillers will likely just burn off the excess supply of rigs created from the last newbuild cycle rather than ordering new rigs, Ms Cook said.

“I think 2024 is going to be that opportunity to finally get the rest of that last newbuild supply out to market. We’ve been sitting on these rigs for a while, and I think we’re finally going to see more of them come out of cold stack and into marketed supply,” she said.

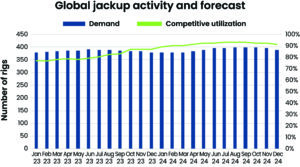

On the jackup side, utilization is expected to remain high over the next two years, primarily due to long-term contracts in key areas. These include the Middle East, India, Southeast Asia and Mexico, according to Matthew Donovan, Senior Rig Analyst at Esgian.

The firm forecasts global jackup demand will increase from 379 units in December 2023 to 387 units by December 2024, with competitive utilization increasing from 87% to 91%. Competitive utilization excludes rigs that are no longer being marketed.

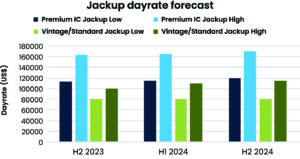

Dayrates are also set to increase slightly for premium jackups, with average dayrates moving from $137,750 in the second half of 2023 to $145,000 in the second half of 2024. Average dayrates for vintage and standard jackups are forecast to rise from around $90,000 to $95,000 over the same time period.

“We’re not seeing new rig orders right now because people are being a lot more careful with their spending, but we’re still early in the upcycle,” he explained. “If you look at global jackup activity, we’ve recovered to the levels we saw just before the last oil price downturn. We’ve recovered in terms of activity and in terms of utilization. Right now, the market looks like it’s going to be strong.”

Latin America

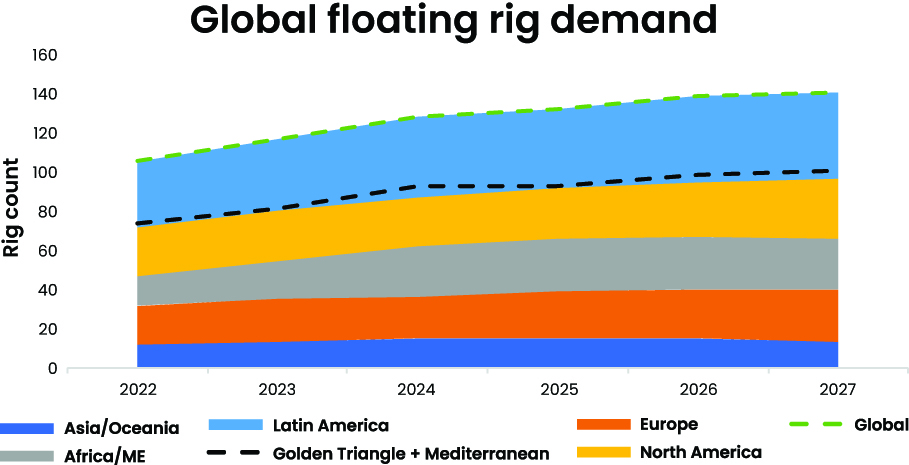

The biggest driver for floater demand heading into next year is still the “Golden Triangle” – the US Gulf of Mexico (GOM), Latin America and West Africa. Wood Mackenzie forecasts this region will account for 75% of global floater demand each year through 2027, averaging between 95 and 100 rigs annually. Latin America will be the leading market, accounting for 35% of global demand, while North America and West Africa will each account for 20%.

In Brazil, Petrobras is adding four additional floaters to its active supply in 2024, for a total of 29 units. That, added to rigs operated by international oil companies, means Brazil will have over 30 floating rigs operating in 2024. With local supply essentially sold out, rigs are now being contracted outside of the region at average rates over $400,000/day.

Petrobras’ aggressive tenders over the past two years proved advantageous in 2023, as the national oil company (NOC) paid an average rate of $271,000/day across its fleet, well below market average for current fixtures on high-spec floaters. Over 75% of its active rigs were contracted prior to the rate escalation seen in late 2022, and those rigs were signed under long-term agreements. In 2024, however, new contracts for the Deepwater Aquila, Pacific Zonda, Valaris DS-8 and Noble Faye Kozack will result in an increase in Petrobras’ average rate across its operating fleet.

“Brazil is the hottest market for the ultra-deepwater rig market right now. We expect Petrobras to contract a few more units over the next 18-24 months,” Ms Cook said.

The Guyana/Suriname Basin will also continue as a major basin in Latin America, though Ms Cook said she doesn’t expect much growth in rig count from Guyana, with ExxonMobil and Hess continuing with the rigs they already have working in the region. The country may add one rig next year to bring the total count from six this year to seven.

Longer-term rig demand in Suriname is more uncertain. Following well appraisal drilling completed in August, TotalEnergies confirmed cumulative resources of nearly 700 million BOE at Block 58’s two main fields, Sapakara and Krabdagu. The operator will begin FEED studies by the end of this year, with the hopes of reaching final investment decision by the end of 2024.

Ms Cook said Wood Mackenzie’s forecast on Suriname has gone down in recent months, primarily due to uncertainty with how aggressive TotalEnergies will be with Block 58. Last year, Wood Mackenzie forecast there would be five rigs in Suriname by 2024, up from one in 2022. This year, the firm has adjusted its forecast to just two rigs for 2024.

However, that forecast may change based on how much additional work TotalEnergies does on Block 58 outside of Sapakara and Krabdagu. Last year, the operator had planned to fast-track development in Block 58, with first oil coming in 2025. However, in its announcement of the FEED study, the operator said first oil would come in 2028 at the earliest.

“A couple of years ago, TotalEnergies was talking about fast-tracking development in Suriname, but now they’re backing off of that. I think the jury’s still out on Suriname and just how big that becomes. You have some other areas that may take the attention away from Suriname,” Ms Cook said.

Africa

Africa’s E&P has gained significant momentum over the past 18 months following exploration successes. Especially with a couple of giant discoveries in Namibia, operators are taking another look at the continent as an area of focus moving forward. These greenfield projects, not only in Namibia but also in Mozambique, Uganda and South Africa, are propping up upstream CAPEX in Africa, even though investments in more mature markets like Angola, Nigeria, Egypt, Libya and Algeria have declined as the risk-reward ratios for operators become less compelling.

Overall upstream CAPEX in Africa reached pre-COVID levels of $40 billion in 2023 and is expected to remain unchanged in 2024, according to Wood Mackenzie.

However, the offshore rig count is forecast to go up by six next year to a total of 26. Utilization reached 100% this year and will remain unchanged next year. “Africa tends to be sold out because there are not a lot of rigs just sitting there,” Ms Cook said.

Namibia is one growing hotspot to look out for in the near-term future, she added. In March, Shell announced a discovery at the Jonker-1X exploration well in the PEL-39 license, approximately 270 km off of the Namibian coast in the Orange Basin. This discovery came a year after the operator found oil in the Graff-1x well and TotalEnergies made a significant discovery in the Venus field, located in an adjacent block in the Orange Basin. These discoveries all lie in water depths of around 2,000-3,000 m.

With Wood Mackenzie estimating these discoveries to hold a combined 6 billion bbl of oil, Ms Cook said the sheer scale will give Namibia an advantage in terms of profitability over other developing regions. Not only will they re-ignite interest in West Africa, but they will also lead E&Ps to explore fields further out on the slope, at water depths where fewer rigs are capable of operating.

“Coming off all the success we’ve seen with Guyana, I think the operators are really motivated with Namibia,” Ms Cook said. “Everyone’s looking for that next highly prolific area. If TotalEnergies or Shell decide to fast-track development, Namibia’s going to grow by leaps and bounds pretty quickly. It’s all about finding those advantaged barrels, and operators are seeking those advantaged areas where they can get the most value out of their CAPEX spending.”

Gulf of Mexico

Transocean announced in July that it will deliver a seventh-generation ultra-deepwater drillship to the GOM for a 1,080-day contract starting in Q4 2025 or Q1 2026. Other than that, much of the news coming out of the region cover extensions or short-term work.

For example, LLOG announced an extension in March for Seadrill’s West Neptune drillship that will keep the rig working in the GOM until Q3 2024. Valaris announced in July a nine-well contract for its DPS-5 semisubmersible for a plug and abandonment campaign that will take the rig into Q1 2024. Announcements like these indicate the GOM will likely remain in a holding pattern for the next year.

Wood Mackenzie is not anticipating a change in rig count for the US GOM heading into 2024 – it is forecast to remain at 25 rigs both for this year and next year. Utilization in the region will also stay at the same level this year and next year – 87% – before moving up to 92% in 2027 as fewer rigs become available in the region.

“Back about 10-15 years ago, we talked about the North Sea as this Steady Eddie – never growing real big but never really declining. Today, that’s what the GOM is,” Ms Cook said. “You’ve got a mixture of supermajors and independents. Half of the rigs are on short-term contracts where they’re coming available, but those independents are using the same rigs over and over again. The other half are the majors who have a little more term on their rigs, so you’re not going to see much change there. That’s how our demand forecast ends up being flat.”

Middle East

The Middle East jackup market remains solid heading into 2024, with NOCs hiking up their CAPEX spending to increase production capacity. Mr Donovan noted that strong demand levels from NOCs, competitive pricing and longer-duration contract terms have driven an influx of jackups into this region from other parts of the world, primarily Southeast Asia, Mexico and China. Esgian forecasts jackup rig count in the Middle East will remain high in 2024, with competitive contracted utilization above 90%. Further, this high level of activity will likely have a residual impact on neighboring markets.

“We’ve just had so many units contracted there since 2021, just a huge amount from the big state oil companies that’s soaked up a lot of the excess capacity in the global jackup market,” Mr Donovan said. “We’ve seen a big shift in jackups moving to the Middle East over the past two years, and those rigs are remaining there to work. That higher level of demand, going forward, is going to keep the market tight in other regions. If you’re doing work in places like West Africa or the Mediterranean, it can be harder to find those jackups.”

Saudi Aramco is one of the key players in the jackup surge. The NOC is in the early stages of a 10-year plan to purchase up to 20 newbuild jackups from ARO Drilling, with the first two rigs expected to be delivered by the end of 2023. ADNOC Drilling also plans to expand its total owned fleet to 142 units by 2024, up from 116 now, supporting ADNOC’s target of raising production capacity to 5 million bbl/day by 2030. In June, ADNOC Drilling announced that it had secured five long-term contracts worth around $2 billion from ADNOC, chartering high-spec premium jackups with battery energy storage systems.

Another significant contract, announced in June, is the 10-year extension of Saipem’s Perro Negro 7 jackup with an operator in the Middle East, worth around $550 million. The drilling contractor noted that it plans to grow its fleet in the region to seven rigs by the end of 2023, up from three rigs in 2021, by purchasing other rigs working in the Middle East market or in neighboring markets.

North Sea

Esgian forecasts jackup demand in the North Sea to go from around 26 units in late 2023 to around 30 units in late 2024.

In the UK sector of the North Sea, Mr Donovan noted that external pressures, like the windfall tax, have made rig demand harder to forecast. The Energy Profits Levy, passed in May 2022 and amended in January of this year, adds a 35% windfall tax on profits generated from operations on the UK Continental Shelf. “The North Sea has seen slower growth than some of the other regions globally,” Mr Donovan said. “A lot of companies, particularly in the UK side, have been slow to up their demand due to the energy profits levy and other pressures. It’s a difficult market.”

In contrast, there are no windfall taxes in Norway on oil and gas profits, and several discoveries there also provide reason for optimism. The first discovery made on the Norwegian Continental Shelf (NCS) in 2023 was Equinor’s Obelix Upflank, which was drilled with Odfjell Drilling’s Deepsea Stavanger semisubmersible 23 km south of the Irpa gas discovery. Obelix Upflank is estimated to be between 2 billion and 11 billion standard cu m of recoverable gas (12.6-69.2 million BOE). Aker BP’s Øst Frigg Beta/Epsilon, which Esgian estimates to be the deepest exploration well ever drilled on the NCS, was drilled in June by Saipem’s Scarabeo 8 semisubmersible to a target depth of 8,168 m and contains an estimated 53-90 million BOE.

Semisubmersibles have been dominating the North Sea market in recent years. However, the jackup market is showing signs of revival heading into 2024. In August, Equinor contracted the Noble Lloyd Noble for a term of 207 days starting in Q2 2024. Options for two additional wells could keep the rig occupied until Q4 2025.

In the UK, CNOOC announced in August it had booked the Shelf Drilling Fortress for a firm duration of four to five months, and options for additional wells with a total duration of about 13 months, which could keep the rig working into early 2025. Harbour Energy also contracted two Valaris jackups and a Noble jackup in the UK, securing rig capacity into early 2026.

However, even with these new contracts, Esgian expects the North Sea to have seven jackups without future commitments – one in Norway and three each in the UK and Denmark. As the semisub market tightens, it’s possible that operators will turn to these jackups to take up some of the work previously done by third- and fourth-generation semisubs. DC