South America offshore market builds momentum with frontier exploration, steady progress

Bumerangue discovery and Morpho well are boosting prospects in Brazil, while LNG projects signal growing potential in Guyana-Suriname

By Stephen Whitfield, Senior Editor

Over the past few years, the offshore oil and gas landscape in South America has undergone a noticeable shift. Traditional fields and proved reserves in areas like the Brazilian pre-salt have matured, while newer plays like Guyana have become consistent producers. Beyond that, new frontiers like the Equatorial Margin in the north of Brazil are emerging as potential growth drivers.

How E&P shapes up on the continent over the next few years will depend on a combination of geological luck, fiscal and regulatory decisions, capital availability, and the ability to build or adapt infrastructure in difficult regions. Overall, however, there is widespread optimism that South America will continue to grow as a major player in the offshore space.

Especially in Brazil, “there is a lot of hope,” said Luiz Hayum, Upstream Research Principal Analyst, Latin America at Wood Mackenzie. “When you look at some of the areas like the south of Brazil, the hope is to find something similar to Namibia. In the north, the hope is finding something analogous to Guyana-Suriname. The question is whether they have working petroleum systems and at the same scale.”

Outside of Brazil, the Guyana-Suriname Basin has been the other region of note in the offshore space in South America. For years, Guyana has been the headline country, with ExxonMobil driving discovery after discovery in the Stabroek Block. However, with new developments on pace to start first oil soon and LNG demand set to drive potential E&P interest in new blocks, Suriname looks set to keep pace.

“Suriname has been very successful in attracting investment,” Mr Hayum said. “They’ve had a lot of success in their licensing rounds dating back to 2020 and 2021, and we’re seeing them get that acreage drilled. We’re on the way to see the first LNG project receive FID.”

Bumerangue: the next major discovery?

One of the top areas of focus continues to be Brazil, where oil became the leading export in 2024 – it accounted for 13.3% of the country’s total exports, according to data released by the Foreign Trade Secretariat of the Ministry of Development, Industry, Trade and Services.

However, the country was starting to face a more uncertain future heading into 2025. Pre-salt production-sharing blocks sold at acreage sales held in 2017-2019 had failed to yield any big discoveries, so the country was still looking to make new, large-scale discoveries that could offset production declines. Brazil could see peak production come as soon as the early 2030s, Mr Hayum said.

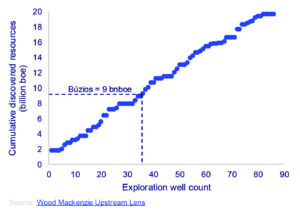

But the Bumerangue discovery in the Santos Basin, announced in August 2025, could change that trajectory. In that discovery, BP said it had found a 500-m oil column below the crest of a reportedly high-quality carbonate reservoir from the 1-BP-13-SPS well.

In its Q4 2025 earning report, BP estimated the discovery held approximately 8 billion boe in place, potentially making Bumerangue the operator’s biggest discovery in 25 years. This could draw additional interest in the region from other operators.

“Bumerangue could change the outlook quite a bit,” Mr Hayum said. “The area where it was discovered is still relatively unexplored, and it’s a very different trend from what we’ve seen over there. That area, in particular, is an area where you’d expect to find much more gas and much higher CO2 levels than what you’d see in the pre-salt layer. It could change some expectations.”

BP reported elevated but undetermined levels of CO2 in the Bumerangue well, so it remains to be seen how commercial the discovery is. High CO2 levels would raise processing costs, making produced volumes more difficult to sell in a lower oil price market. An appraisal well is expected to be drilled in early 2027.

Prior to that, BP is also planning to drill an exploration well in the Tupinambá block, located near the Bumerangue block in the Santos Basin, in the second half of 2026. If hydrocarbons are found, the company may drill two additional wells on the block before the end of the year.

“The wells that are going to get drilled in late 2026, early 2027 are the key wells to unlocking this region,” Mr Hayum said. “If some of BP’s expectations are confirmed – and they’re expecting very extensive reservoirs of good-quality rock and manageable CO2 levels – it puts more optimism into a region that’s perceived as very high risk. If that risk looks lower, that’s going to attract more drilling. You have some second-order blocks around Bumerangue and Tupinambá, other opportunities to license out there, and the companies looking to get access to this acreage will be watching to see how the risk profile changes.”

Equatorial Margin: the next frontier?

Mr Hayum also noted Brazil’s Equatorial Margin as one of the country’s last remaining offshore exploration frontiers, with operators expecting to find similar oil and natural gas deposits as those found offshore neighboring Guyana and Suriname. The Foz do Amazonas Basin is located off the coast of Amapa state on Brazil’s maritime border with French Guiana and along a similar geologic trend as discoveries made offshore Guyana and Suriname.

Exploration in the Equatorial Margin had been at a virtual standstill since 2017, when the Great Amazon Reef System was discovered at the mouth of the Amazon River. Environmental and indigenous groups have since pressured the Brazilian Institute of Environment and Renewable Natural Resources (IBAMA) and the National Agency of Petroleum, Natural Gas and Biofuels (ANP) to deny drilling permits in the region.

In 2025, however, IBAMA granted Petrobras a permit to drill an exploration well (Morpho) in the FZA-M-59 block of the Foz do Amazonas Basin, the first exploration well in the Equatorial Margin since 2015. Drilling of the Morpho well, planned for a total depth of 7,000 m, was being executed by the Foresea-owned ODN II drillship and planned for completion in Q2 this year.

In addition, Petrobras holds operating stakes in 16 blocks spread across the Barreirinhas, Ceará, Foz do Amazonas, Pará-Maranhão and Potiguar Basins. The company announced plans to spend $3 billion to drill Morpho and an additional 14 wells in the Equatorial Margin under its 2025-2029 investment plan.

Mr Hayum described the Equatorial Margin as a source of cautious optimism for other operators eyeing a new frontier. The award of a permit for Petrobras to go ahead with the drilling of Morpho laid out a roadmap for E&Ps to follow in obtaining permits. This resulted in renewed interest in the region at Brazil’s Open Acreage concession auction last June.

Concerns about development in an environmentally sensitive region still remain, however, and Mr Hayum noted that it will likely be challenging for Petrobras to move as quickly in the Equatorial Margin as ExxonMobil has moved in Guyana.

“It took years to get a permit to drill a single well,” he said. “And it’s not only the wells. For a development, you need to build offshore support spaces. You have a whole movement of support vessels, helicopters and paving roads.”

Further, Mr Hayum cautioned against expectations of immediate success from exploration wells in the Equatorial Margin, even in the best-case scenario where the region finds reserves similar to Guyana-Suriname.

“It took Guyana a while before they found the trend. Many operators had several failed wells before it hit. I wouldn’t see Petrobras necessarily stopping if they don’t hit on the first well, but you need to see the results. You look at Guyana, that was really favorable geology, and it was an operator that moved fast and could do the exploration, appraisal and development simultaneously. Petrobras will need a lot of coordination to replicate that success.”

If Petrobras’ efforts in the Equatorial Margin bear fruit, Mr Hayum said even more majors could easily become involved in future Open Acreage auctions: “The area makes sense for any of the deep-pocketed explorers. You look at the other majors that are already in Brazil like BP, Shell and Equinor, they’re looking to reload exploration acreage. The Chinese NOCs are also quite strong in the pre-salt, so they could be interested. For any operator already working in the pre-salt, it would be a natural movement to head into this area.”

Guyana-Suriname: A period of transition

For the Guyana-Suriname basin, LNG offers an offramp for E&Ps to realize the value of notable discoveries with a lot of gas. Wood Mackenzie estimates that Guyana’s Haimara cluster and Suriname’s Block 52 hold 13 trillion cu ft of discovered non-associated gas. These sources could deliver a potential LNG supply at a breakeven of around $6/million Btu. This comes at a time, the firm noted, when the global market still needs 105 million tonnes/year of pre-FID LNG to fulfill a global supply/demand gap by 2035, according to Wood Mackenzie.

In Guyana, ExxonMobil confirmed on 19 March that it had submitted a field development plan for Project 9 in the Haimara field, located in the southeastern portion of the Stabroek Block.

In Suriname, Petronas has targeted a 2026 FID date for a floating LNG project that would tap the Sloanea field in Block 52; this followed Suriname NOC Staatsolie’s confirmation of the commerciality of the Sloanea-1 well last year.

“With Suriname, you have multiple stacked reservoirs with different fluid qualities. Some of them will have a lot of gas. TotalEnergies could do the work to find a new cluster that could be targeted for development, but as you move into Block 52, they found a lot more gas. This development with LNG is good news for the area,” Mr Hayum said.

The LNG project, if sanctioned, would be the second E&P project to start offshore Suriname, following the TotalEnergies-operated GranMorgu project in Block 58 set for first oil in 2028. Mr Hayum cited the willingness of Staatsolie – which also holds regulatory power for the country’s petroleum sector – to negotiate favorable fiscal terms with international partners as a positive sign for the future.

“The big thing with the LNG in Block 52 is that Petronas is working along with Staatsolie on improving the terms to make the project viable,” Mr Hayum said. “When you have an experienced regulator that’s pragmatic and can work with the offshore operators, that’s going to lead to some success, so we’re optimistic there.” DC