Analysis: Sustained supply disruption could reduce global oil demand by 20% and gas by 10% by 2050

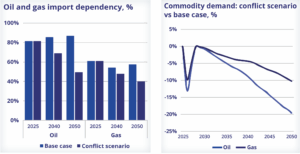

Prolonged disruption to Middle East energy supplies could accelerate a structural shift in global energy systems, halving oil and gas import dependence by 2050, according to Wood Mackenzie. Further, as countries prioritize energy security, oil demand could be cut by 20% while gas demand is cut by 10%. This would be due to countries increasingly meeting energy demand through electrification, renewables, coal and nuclear.

The analysis, which assumes a major geopolitical escalation disrupting 15–20% of global oil and LNG supply, indicates that oil demand falls by around 9% in the near term due to supply outages. That demand recovers to pre-crisis levels by 2030.

Beyond 2030, structural shifts take hold as countries accelerate efforts to reduce reliance on imported fuels. Oil and gas demand declines more rapidly than in the base case, as governments prioritize domestic and diversified energy systems.

“Geopolitical crises can act as powerful catalysts for long-term system change,” said Prakash Sharma, VP Scenarios & Technologies at Wood Mackenzie. “In this scenario, the world moves decisively towards energy independence, with lasting implications for global fuel demand and trade.”

Electrification and efficiency emerge as the primary pathways to energy independence. Overall power demand remains broadly in line with the base case, as lower demand from electrolytic hydrogen production is offset by wider electrification across transport, buildings and industry. This shift reduces reliance on imported fuels while maintaining overall energy service demand.

By 2050, the global energy mix shifts significantly under the conflict scenario:

- Oil demand falls 20% and gas 10%, while coal rises 20% as countries diversify supply and prioritize domestic resources.

- Nuclear generation increases 40% above the base case.

- Renewables continue rapid expansion, forming the backbone of domestic power systems.

- Hydrogen and carbon capture adoption declines, as policymakers favor more efficient and secure energy pathways.

This means coal is expected to play a larger role in the near term as countries respond to supply shocks by maximizing domestic energy sources and delaying plant retirements. Over the longer term, nuclear expands significantly, providing stable, fuel-secure baseload power as new capacity comes online from the 2030s.

Gas-fired power and hydrogen-based abatement pathways are scaled back as energy systems favor more secure and proven alternatives.

UKCS corporate landscape shifts as majors retreat

On 30 March, the merger of NEO NEXT with TotalEnergies was completed, forming NEO NEXT+. The merger highlights the emergence of UK-focused players, replacing the dominance of the majors on the UK Continental Shelf (UKCS), according to Westwood Global Energy Group.

NEO NEXT+ is now the largest UKCS company based on 2026 net production, Westwood’s analysis indicated. The company ranks as the second-largest based on net remaining reserves, behind Adura, the Equinor and Shell joint venture.

The merger signals another step in the evolution of the UKCS. In 2014, the five largest companies in terms of remaining reserves were all majors – Shell, BP, Total, ConocoPhillips and Chevron – with Apache occupying sixth position. These six companies accounted for 44% of the UKCS remaining reserves. But the oil price crash in 2014 started a shift in strategy for many companies. By 2020, a new generation of companies had emerged in the UK, backed by private equity and private financiers. BP, Shell and TotalEnergies remained in the top six, but Chrysaor (now Harbour Energy), Equinor and Ithaca Energy replaced ConocoPhillips, Chevron and Apache.

In 2026, for the first time in decades, the only major within the top six companies on the UKCS was BP. Since 2014, the majors’ direct share of UKCS reserves has fallen from 52% to 16%. The mergers of significant players in the UK now means that the top six companies – Adura, NEO NEXT+, Ithaca Energy, BP, Harbour Energy and Serica Energy – account for 80% of remaining reserves. Four of these six companies are focused on UK portfolios, with only BP and Harbour Energy holding international portfolios.

The total number of companies holding reserves on the UKCS has also fallen drastically. In 2014, there were 74 companies holding reserves, but by 2018 this had fallen to 63. Today, only 34 companies remain, reinforcing the extent of consolidation now characterizing the basin, Westwood’s analysis stated.

Click here to read more about the UKCS market outlook.