Analysts maintain optimistic outlook for onshore drilling market, but uncertainties remain

Rig counts and wells drilled are expected to increase in 2023, but market still remains in flux due to supply chain, geopolitical factors

By Stephen Whitfield, Associate Editor

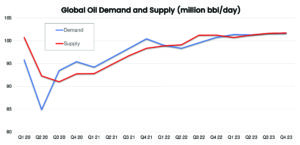

In the face of a potential global recession in the coming year, coupled with continuing supply chain pressures, outlook for the global onshore drilling industry remains murky – but mostly favorable. The good news is that outlook for oil prices remains strong. Even though WTI prices have settled down from an average of $127 in March 2022 to $89 as of 14 October, it is still expected to remain in that range over the coming year, supported by strong energy demand as more countries open up post-pandemic and with Russia’s production under question due to the continuing conflict with Ukraine.

Between Q3 2022 and Q3 2023, WTI will likely trade at between $75 and $110, according to John Spears, President of Spears and Associates. He expects the Henry Hub gas price to decrease from $7.50/mmBtu to $6.30/mmBtu in the same time span. “We’re assuming that there’s going to be a recession and, more importantly, we’re assuming that any economic recession is going to result in a reduction in oil demand,” Mr Spears said. “But that’s not nearly as straightforward as you might imagine because more than half of global oil consumption now comes from emerging markets. Their demand is not tied so much to economic cycles as it is to urbanization and industrialization. So, there’s a possibility that oil demand might go up anyway. If that’s the case, that could push prices higher.”

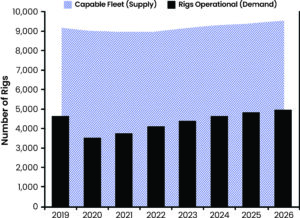

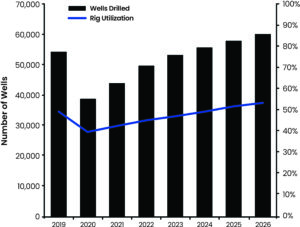

The global onshore rig count is expected to average 4,070 by the end of this year, which would already represent an 18% increase from the 2021 average of 3,450, according to Westwood Global Energy Group. By the end of Westwood’s forecast period in 2026, that rig count is expected to increase by an additional 24% to 5,050 rigs. Total wells drilled are also expected to rise from 49,600 in 2022 to 60,000 in 2026.

“If you’re a drilling contractor and you’re hearing about the operators and their free cash flows, that’s certainly good news. Maybe there’s some ability to add on additional services,” said Luke Smith, Analyst at Westwood.

North America onshore outlook

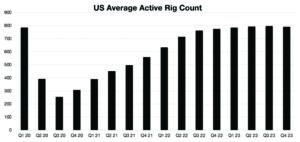

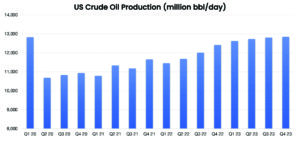

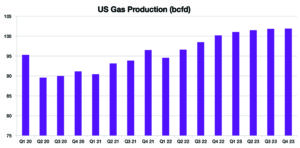

Mr Spears projects US onshore rig count will average 705 in 2022 – up from 460 in 2021 – and go up to 770 next year. Wells drilled is expected to average 19,500 in 2022 and go up to 21,400 in 2023. Lower 48 onshore dry gas production could increase from 94.3 billion cu ft/day in 2022 to 97.6 billion cu ft/day in 2023. This would essentially bring drilling activity back to the level he originally projected the US market to reach in 2020, prior to the downturn. However, the industry that’s emerged from the downturn is not the same as what existed before. Operators are focusing more on returning free cash flow to shareholders instead of chasing additional growth.

This focus on capital discipline will likely have a trickle-down impact on the rig market. Average asset utilization for US onshore will likely end up falling between 80-85% this year, and Mr Spears said he does not expect any significant change in 2023. For drilling contractors, their continued focus on capital discipline means they are unlikely to bring newbuild rigs into the market to meet demand.

“The operators and service companies have been restructuring their balance sheets so that they’re less burdened by debt. Because of that, they’re going to be less volatile, which means growth is probably not going to be as high as it might have been before the last downturn,” Mr Spears said.

In Q3 2022, leading-edge dayrates were approaching the low-$30,000 range, a 25% increase from Q3 2021. However, Mr Spears said he does not expect that number to increase significantly in the next year. At most, he anticipates average dayrates for US onshore to reach $32,000 in 2023 – primarily because drilling activity is not expected to grow at the same rate as it did in 2022. “If things flatten out on the activity side like we think they’re going to do, I don’t see how we get a lot of movement on dayrates. The upward movement in dayrates has been all about rising asset utilization, but now most of the high-spec rigs are under contract.”

As usual, the Permian Basin remains the primary driver in US onshore activity, and that is expected to continue into 2023. Mr Spears estimated a 10% increase in the basin’s rig count over the course of the year, from 342 in 2022 to 376 in 2023, while wells drilled will also see a 10% increase, from 8,150 in 2022 to 9,000 in 2023.

Permian activity could see a boost due to the planned addition of five natural gas pipeline projects. If completed as planned, they will increase the Permian’s takeaway capacity by a total 4.18 billion cu ft/day over the next two years, according to the US Energy Information Administration (EIA). Three of these pipeline projects – Kinder Morgan’s Gulf Coast Express Pipeline Expansion and Permian Highway Pipeline, and Whistler Pipeline Capacity Expansion led by Whitewater and the MPLX joint venture, are expected to come on stream in 2023.

Any delays in the construction or permitting for these pipelines could negatively impact the forecasted drilling activity growth, Mr Spears said. “It takes a long time to get a pipeline built, even in the state of Texas, so that’s a bit of a wildcard: How soon can we get to full utilization on the pipeline side out of the Permian?”

Besides the Permian, the industry can also look to the Haynesville Shale for some additional drilling activity next year. Mr Spears projects a 15% increase in rig count there, from 66 rigs in 2022 to 76 in 2023, and a similar increase in wells drilled, from 700 in 2022 to 800 in 2023.

Like with the Permian Basin, growth in Haynesville depends heavily on takeaway capacity. The basin has already seen an increase of 1.3 billion cu ft/day in takeaway capacity over the past two years, according to the EIA.

This can be attributed in part to three pipeline projects that were completed in 2021: The Enterprise Product Partners’ Gillis Lateral pipeline and its associated expansion of the Acadian Haynesville pipeline, along with Enbridge Midcoast Energy’s CJ Express pipeline. These pipelines have allowed producers to reach industrial demand centers and LNG terminals on the Gulf Coast, making the Haynesville a more attractive drilling location.

“The Haynesville is all about gas, and the fact that gas prices this year are going to average $8 means it makes sense to drill gas wells there, so the region can accept more rigs. It’s well positioned with regards to access to pipelines, and as a supply basin to both export markets for LNG as well as domestic industry,” Mr Spears said.

While pipelines and LNG terminals are helping to spur growth in some of the big shale plays in the US, the lack of this midstream infrastructure is hindering onshore drilling growth in Canada.

Mr Spears said he expects just a 2% growth in Canada’s onshore rig count next year, from 178 rigs in 2022 to 182 in 2023. The country has hit a bottleneck, he noted, where it cannot export enough oil and gas to justify an increase in production because of issues with approving new pipelines into the US, along with the high cost of oil sands development and a lack of LNG terminals. The country’s first two LNG terminals, the Shell-led LNG Canada project and the McDermott-led Woodfibre project, are not expected to come on stream until 2025 and 2027, respectively.

“The issue for Canada is that, on the land side, their big market for oil and gas exports has been the US. With US production growing for both oil and gas, plus the lack of LNG terminals Canada has in place, it’s tough. They’re not going to have an LNG terminal up and running for a while. It’s going to be that way for another two or three years.”

Global onshore outlook

Outside of North America, China and the MENA (Middle East and North Africa) regions are expected to be among the key drivers of onshore rig activity in the near term.

In China, NOCs that operate the country’s largest oil fields are aiming to increase both oil and gas production, leading to increased activity in the country’s shale oil deposits. In July, Sinopec announced a major oil discovery in the Subei Basin, and PetroChina sanctioned a development plan for shale gas extraction at the Yang 101 Block in the Sichuan Basin. Over the next three to four years, Westwood forecasts these two projects will help drive onshore rig count from 1,210 in 2022 to 1,440 in 2026, and the onshore wells drilled over that time period should jump from 14,200 in 2022 to 16,120 in 2026.

In the Middle East, Westwood forecasts onshore rig count to increase from 580 in 2022 to 730 in 2026, while onshore wells drilled are forecast to go up from 3,310 in 2022 to 3,900 in 2026. Saudi Arabia and the UAE will be the main drivers of activity growth, with their NOCs announcing ambitions for increasing production capacities by 2030.

“When you look at the Middle East and China, the high oil prices we’ve seen this year certainly helped solidify their long-term national strategies,” said Ben Wilby, Senior Analyst at Westwood Global Energy Group. “Saudi Arabia wants to get to 13 million barrels, the UAE wants to get to 5 million barrels, and China wants to reduce its imports.”

Argentina is also expected to be a bright spot in the onshore market, in anticipation of the launch of the country’s new pipeline in the Vaca Muerta in 2023. Rig count there has already increased from 38 in 2021 to 87 in 2022, and Westwood expects that number to hit 113 by 2026. Number of wells drilled could reach 1,200 by 2026, Mr Wilby said, adding that these projections are “bearish” and could go higher if the pipeline launches on schedule.

Russia, bogged down by its invasion of Ukraine and geopolitical pressures, has already seen a notable drop in drilling activity this year. The number of wells drilled has dropped by almost 28% in 2022 compared with 2021. This decline is expected to continue into 2023.

US and Western Europe’s sanctions on Russian oil and gas have certainly contributed to this decline, as have the departure of several operators and major service companies, all announced this year. BP cut ties with its 19.75% shares in Rosneft, while Equinor announced it will exit its Russian joint ventures, including the North Komsomolskoye development project in West Siberia and 12 E&P licenses in East Siberia.

Shell also ended its involvement in the Nord Stream 2 pipeline and dropped its 50% shares in the Gydan and Salym development projects. Schlumberger, Halliburton and Baker Hughes all announced plans to suspend new investments in Russia following the invasion. On the drilling contractor side, KCA Deutag has suspended new investments and is evaluating options on its 21 rigs located in Russia.

In the EU, which is facing something of an energy crisis due to its reliance on Russian gas, countries are now scrambling to find new sources of energy. In the near term, this is unlikely to lead to a significant increase in rig count. Mr Wilby forecasts Western Europe will only have six onshore rigs in operation next year, the same as last year. That could change in the longer term, with the UK government’s recent decision to end its moratorium on hydraulic fracturing, as well as news that Shell may have discovered major shale reserves in Block 2 and Block 4 in the southern part of Albania.

However, it is more likely that Europe will boost its gas imports through pipelines from Africa. In July, the Energy Ministers of Algeria, Niger and Nigeria signed a memorandum of understanding to set up a task force for building the Trans-Saharan Gas Pipeline, which would deliver natural gas from Nigeria to Spain.

“There’s certainly an appetite we haven’t seen before, and that’s because Western Europe is just desperate for natural gas,” Mr Wilby said. “However, the reaction we have seen from the region is not one of increasing domestic drilling activity. Instead, they are seeking alternative supply outside of Russia. There is some potential for some projects in Western Europe, but whether that will translate into anything, it is hard to say.” DC