UK offshore industry calls for policy changes that face market realities

Windfall tax, lack of new licenses among key hurdles to be removed for UK to revitalize a stagnant E&P industry, meet rising energy needs

By Stephen Whitfield, Senior Editor

Heading deeper into the latter half of the 2020s, the offshore oil and gas industry in the UK is at an inflection point. The country will continue to need significant volumes of oil and gas for decades. According to Offshore Energy UK’s (OEUK) Business Outlook Report 2026, oil and gas still supplied 75% of the country’s energy needs as of January 2026. And by 2050, even presuming the UK meets its net zero ambitions, oil and gas will still account for 20% of demand.

The report also noted that the UK is projected to need a total of 10-15 billion boe between 2026 and 2050. However, the country is currently on pace to produce only 4 billion boe in that time frame. Without active investment in domestic production, the nation will become highly dependent on imports.

Yet recent government policy actions have not supported such investments. In fact, industry stakeholders say that the country’s regulatory and fiscal regimes are actively stifling business confidence and the potential for investment into drilling. For the first time in decades, no new exploration wells were drilled on the UK Continental Shelf (UKCS) in 2025.

One of the key policies currently in the crosshairs is the Energy Profits Levy (EPL), a 38% tax on profits from oil and gas E&P on the UKCS. Commonly referred to as the “windfall tax,” the EPL was introduced in May 2022 following surging energy profits driven by the Russia-Ukraine conflict. It pushed the headline tax rate for North Sea oil and gas to 78%. Industry advocates such as OEUK have argued that such high tax rates have hindered investment and the market’s competitiveness. Moreover, the tax has increased project uncertainty for E&P companies, which is delaying investment in the industry’s supply chain capability and resources.

“There’s been a chilling effect on investments – not just investment from operators in the region but also within the energy supply chain,” said Katy Heidenreich, Supply Chain and People Director at OEUK. “The Energy Profits Levy is one of the big challenges impacting supply chain confidence. Companies are asking, can they grow their business here? More companies are looking overseas, away from the UK.”

In its Business Outlook Report 2026, OEUK noted that last year saw the lowest level of well activity since 1964, the earliest year of record. Only two appraisal wells were drilled and, for the first time on record, zero exploration wells were drilled. Drillers in the region, understandably, are deeply concerned about where the industry is heading.

“It’s impacting our drilling contractors and the supporting supply chain from start to finish,” said Stuart Sutherland, Vice Chair of the IADC North Sea Chapter, noting that no exploration wells have been planned for 2026 either. “We’ve got to consider that the cost of extracting and uplifting a barrel in the UK is now higher than anywhere else in the world. That’s a reality we need to start facing.”

Industry stakeholders agree that, despite the current decline, there is still significant potential to boost production on the UKCS, but that depends on having supportive fiscal and regulatory policies over the next few years. Moreover, the window for changing the industry’s trajectory is not going to stay open forever, as current policies could have irreversible consequences if left unchanged for too long. The failure to attract investment in new fields risks the early closure of North Sea infrastructure, for example. Once that infrastructure goes, there may not be any more opportunities for an industry rebound.

“There are a lot of brilliant opportunities for us to get after in the North Sea,” Ms Heidenreich said. “We could be self-reliant on natural gas. We could meet up to half of our own energy needs. We just need a supportive, growth-driven regulatory regime. And we need a fiscal regime that is stable and that companies can plan around.”

The problems with the windfall tax

In February, the North Sea Transition Authority (NSTA) released projections showing a sharp decrease in E&P CAPEX over the next five years, from £13.74 billion in 2026 to £9.19 billion in 2031. This forecast presumed an average Brent price of £52.4 per barrel of oil equivalent (boe), the same as the 2025 average. It also forecast that CAPEX for exploration and appraisal would drop by more than half in this period, from £240 million in 2026 to £110 million in 2031.

But the trend had already been going downwards for the past few years, as highlighted by the OEUK’s 2026 report. For one, the industry is shrinking to fewer major players. In 2019, the top five producing operators accounted for just 50% of total production, but by 2025, the top five accounted for more than 70% of production. Return rates on investments have also been discouraging for UK operators, averaging -2.6% from June 2024 to June 2025. In fact, the report noted that there were seven consecutive quarters (Q4 2023 to Q2 2025) of negative rates of return, which is the longest sustained period of negative returns on record for UKCS companies.

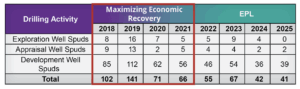

Regulatory and fiscal pressures, along with the future uncertainty those pressures have amplified, have been key factors behind these trends. For the drilling sector in particular, the OEUK noted that the impact from regulatory changes is clear. In 2016, the UK government had launched its Maximizing Economic Recovery (MER) regulatory strategy, with the aim to achieve the maximum value of petroleum recovered from the UKCS.

This policy had a “profound” effect on well activity, according to the OEUK report, which noted that it preceded a strong period of domestic oil and gas production. The formation of the NSTA in 2015, a central tenet of the MER strategy, helped usher in growth in exploration, appraisal and development drilling. From 2018-2021, the UKCS averaged 95 well spuds per year. However, after the EPL was implemented in 2022, the average dropped to 51 well spuds per year for the next few years.

But the challenge with the EPL is not just about pushing up the headline tax rate and making projects economically unfeasible, Ms Heidenreich said. It’s also about the increased uncertainty and the inability of companies to make long-term business plans. There have been multiple changes to the EPL since its introduction, including an unexpected 3% increase in 2023 and the removal of an investment allowance designed to encourage investment in UKCS E&P that same year. In 2024 and 2025, the government also unexpectedly pushed back the end date of the EPL. All of these actions have led to a high level of fiscal uncertainty in the industry, further pushing producers to scale back on drilling campaigns in the UK and to shift capital to other countries with more stable and favorable tax regimes.

“Companies need confidence that the tax isn’t going to change in two or three years’ time, or that it won’t change if a new political party comes into leadership. With this industry, you’re making decisions around projects that are going to be around for 10 to 15 years. You need certainty to make those investment decisions,” Mr Heidenreich said.

Currently, the EPL is set to expire on 31 March 2030, or earlier if oil and gas prices fall below a certain threshold under the Energy Security Investment Mechanism. For the 2025-2026 fiscal term, that price threshold is $76.12/bbl for oil and £0.59/therm for gas (a therm is equal to approximately 100 cu ft). At that point, the tax would be replaced by a permanent tax called the Oil and Gas Price Mechanism (OGPM), which will apply only during periods of high oil and gas prices – and those specific thresholds are yet to be determined. The UK Treasury Department has said it would consider the costs associated with commercially viable projects in setting the initial thresholds. After that, the thresholds would be adjusted using the Consumer Price Index, similar to how the current EPL price mechanism is adjusted.

OEUK has advocated for the government to transition to the OGPM before 2030, noting that early discontinuation of the EPL could positively impact the oil and gas industry and the UK’s energy landscape.

Last year, the organization conducted a survey among its operator members, asking about projects that are not currently being pursued but they would consider if the EPL were reformed in 2026. The surveyed operators highlighted 111 projects that fit this category, which would call for an additional £50 billion in private capital investment and lead to 3.5 billion boe in production. Developing these projects could nearly double the UKCS’ output over the next 25 years, according to OEUK.

The OGPM would also create a more predictable and less punitive structure than the current windfall tax. By going into effect only when oil and gas prices are above a certain threshold, it would effectively tax only the windfall revenue. This would provide greater fiscal clarity and more stability going forward, Ms Heidenreich said, enabling companies to better plan their businesses.

“This mechanism shows that the government has very much listened to industry, and they understand what a supportive fiscal regime looks like,” Ms Heidenreich said. “It’s something that will work for industry. The biggest thing for us is that it will be a permanent mechanism, so companies can have confidence that it’s not going to change.”

The problem with licensing

Even if the UK government ended the EPL today, however, the UK’s upstream industry would not suddenly rebound to its heyday. A lot of other work remains to be done to reverse the decline of drilling activity in the country.

That has been one of the key messages pressed by the IADC North Sea Chapter. Mr Sutherland, who assumed his current role as Vice Chair in 2025, pointed to the Labour government’s stance on new North Sea oil and gas licensing as a huge obstacle. In November, the government issued its North Sea Future Plan, in which it outlined a ban on new licenses for oil and gas exploration. This decision, which came a year after the Labour Party’s win in the 2024 general election, marks a significant policy shift from the MER strategy, introduced under the previous Conservative government.

“Right now, there is no commitment for the government to issue any new licenses for exploration,” he said. “Before we make any progress, we need to see a step in that direction. We need to start allowing new wells to be explored and new fields to be developed. That’s not a 2026 outlook – it’s a 2027, 2028, 2029 outlook and beyond. We need continuity of work, where contracts can be put in place that brings rigs back to the UKCS.”

In a mature basin like the North Sea, he added, a steady flow of investment and new licenses is necessary just to keep production at a standstill. Without ongoing activity, decline accelerates and import dependence rises more quickly. This, Mr Sutherland said, is why countries like Norway and Denmark continue to license and develop new projects. Their approach allows them to replace what they produce and manage decline more effectively.

“When you look at a country like Norway, they’ve got major projects in the pipeline and major infrastructure being built. That didn’t happen overnight – it’s the result of a long-term strategy of investment that supports energy production, generates revenue and enables reinvestment into lower-carbon energy resources. We’ve got the same geology here in the North Sea. There’s no reason we can’t build out that kind of infrastructure. Everybody looks at Norway and Denmark and what they’ve done, and we’d like to go in that direction. But that requires long-term commitment, investment and trust – both in government and from the general public,” he said.

In its 2025 Licensing and Infrastructure Report, which was published using data from Westwood Global Energy Group, OEUK argued that there remains substantial upside in unlicensed acreage on the UKCS. The report estimated that 46% of liquids resources on the UKCS lie in unlicensed acreage.

Moreover, even if the UKCS is a relatively mature producing region, there are fields that are still underexplored, and individual developments could materially shift regional output. Mr Sutherland pointed to the Equinor-operated Rosebank development as an example, which is set to start production in 2027 in the West of Shetland basin offshore Scotland. The Ithaca Energy-owned Cambo near-term development and the BP-owned Clair South are other developments that could boost production out of that basin, although those fields have yet to be developed. A lack of new licensing rounds is a key barrier for operators, as they don’t have the opportunity to further assess the acreage.

“Our infrastructure investment is just not there right now,” Mr Sutherland said. “We’d have to really focus on getting back to investing in that oil and gas infrastructure. You need a licensing round to get approved, you need new fields to get approved, you need a year of tendering and you need a rig. Drilling infrastructure takes a minute to get together.”

With the UK’s next general election set to be held no later than 2029, the Labour government’s opponents have already put forth their own plans with licensing. The Conservative Party, which was previously in power from 2010-2024, has unveiled its Cheap Power Plan. Among other things, it would open up new licenses for exploration drilling on the UKCS, as well as repeal the EPL. Reform UK, a right-wing populist party, has pledged to fast-track North Sea oil and gas licenses if elected.

Mr Sutherland said such policies would be hugely beneficial for drilling contractors, as they would incentivize operator investments. However, he cautioned that the industry would need time to see such a policy shift take hold. The government would need to maintain a consistent message promoting industry growth in order to make the UK an attractive region for E&P.

“We’re not suddenly going to go back to an attitude of ‘drill, baby, drill,’ ” Mr Sutherland said. “That’s not going to happen, and I think we, as drilling contractors, recognize that. Still, consistency is key. Clients don’t believe what governments say. Two years ago, there was a clear position of no further exploration. Even if that position changes, investors will still ask what happens after the next election?”

The problem with messaging

Paul Brown, European and Mediterranean Regional Commercial Director for OES Asset Integrity Management, noted another hurdle in building back the UK’s drilling industry. Even if the EPL is abolished and new licenses for drilling are approved, it will be a challenge to find enough people to do the work.

Mixed messaging about the future of oil and gas in the UK has created hesitation among early-career professionals about whether the industry is a viable long-term option. This is posing substantial recruitment problems for an industry that needs to fill skills gaps and build a talent pipeline for the future, he said. Mr Brown previously served as Associate Member Vice Chair for the IADC North Sea Chapter.

The jobs market, as described by Mr Brown, is a bit of a vicious cycle. Energy sector employers have had to reduce their staff headcounts due to a declining market, while more young people are choosing other industries when they see the layoffs and declining market. The lack of a workforce pipeline then makes it less attractive for companies to invest in the region.

Other government policies have also contributed to the challenge. Mr Brown cited a 2025 increase in the rates at which employers must contribute to the national insurance, from 13.8% to 15%, and the lowering of the salary level at which employers must start paying into insurance, from £9000/year to £5000/year.

“Our industry has gone from almost a guaranteed job to something else. We’re losing a lot of jobs every month. The scary thing for us is this idea of replenishing the workforce. Whereas traditionally, companies would take on trainees and apprentices, we’re in an environment where entry-level jobs here are incredibly expensive, and that makes it risky to employ new people. Combine that with everything else going on, and that makes a perfect storm,” Mr Brown said.

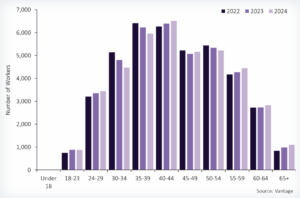

At the same time, the current oil and gas workforce continues to age and retire. According to OEUK’s Workforce Insights 2025 report, the average age of offshore oil and gas workers is 44, but there has been a 25% increase in the number of workers ages 65 or older from 2022 to 2024 (the three-year period in which data was measured). As these workers retire or leave the industry, there is a risk of losing vital skills, knowledge and experience that could disrupt operations.

“If we can’t recruit young people, who’s going to do my job in 20 years?” Mr Brown said. “We’ve got an aging skillset where a lot of the guys that were there in the 1980s and 1990s are retiring. The companies that are involved in drilling out here are either not recruiting or struggling to recruit. We don’t have the universities spitting out graduates who are going straight to the drillers and the operators. They’re told there’s no future in oil and gas. We’ve got to reverse that narrative. We know there’s going to be oil and gas for at least the next 50 years.”

Building back the workforce will take a multi-pronged approach, Mr Brown said, with government policy playing a key role. Reforming the EPL and addressing oil and gas licensing will create greater investment certainty, which would then have a downstream effect – greater operator confidence and investment would lead to more work for drilling contractors, and more drilling work would encourage them to invest more in recruitment. Outreach to colleges and universities is also vital to attracting new talent.

But beyond that, Mr Brown said he hopes to see changes to the public discourse around oil and gas – with the industry becoming more vocal about the value it provides to the UK energy market. For instance, the public needs to be able to see a direct connection among the country’s rising energy prices and domestic energy production and energy independence.

“The issues with this industry are still very much an internal conversation, but the one thing that’s really gaining traction outside of industry circles is energy prices,” Mr Brown said. “Why are we paying the highest energy prices in the world for our houses? Why are we getting more energy-efficient boilers and equipment, but the cost of energy is so much more expensive? Something’s not adding up, and many people are feeling the squeeze.” DC